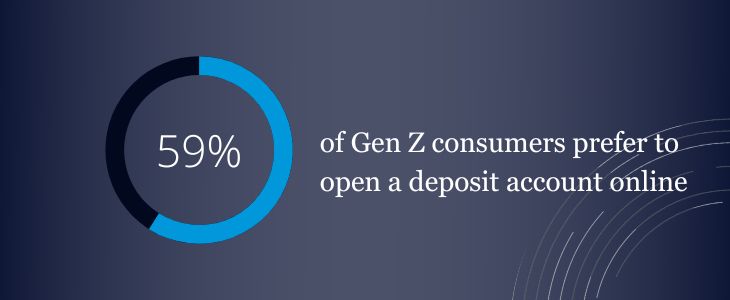

A Look at Gen Z Banking Habits and Attitudes

Compared to other generations, fewer Gen Z customers expect to remain with their primary financial services organization a year from now. Do you know what Gen Z wants?

They are mobile-centric, diverse, ambitious and just starting their careers. They also have strong opinions on what they expect from their financial services organization. Our BAI Banking Outlook Special Report shares essential insights on Gen Z, the newest generation of banking customers.

Source: BAI 2022, www.bai.org

Insight: The Disruptive Threat

Insight: The Disruptive Threat

By now, everyone in Financial Services has seen a headline with dire warnings of “disruption” – by one of the Internet Giants like Amazon or Facebook, or by a regional FinTech startup in Australia. Industrie&Co’s Lukas Bower explains how financial services providers can respond to the disruptive threat.

How can you Respond?

The disruptive threat is indeed real, but how does a mid-tier financial services provider respond?

Many mid-tier providers in Australia focus on a specific region, industry, or some other slice of the broader market. To combat disruption, your solution lies in uncovering and addressing a need that is uniquely important to your specific community of customers.

The “Design Sprint” Approach

If you read the trades, you’ll be aware that customer-centricity is the norm in today’s digital business.

Early customer-centric methodologies focused on the desirability of an idea – exploring whether a customer wants a new feature, by testing an idea with real customers.

As customer-centric approaches have matured, they have expanded to look at technical feasibility and commercial viability as well. This end-to-end exercise is called a Design Sprint – which can be completed in a matter of weeks.

Feasibility & Viability

Feasibility explores your existing technology landscape (CMS, CRM, and any other customer-facing systems), and determines if an idea customers love is technically feasible to implement. Feasibility considers your existing environment – and calls out any technical gaps that need to be addressed. If gaps exist, the feasibility phase tests whether they can be addressed through short Tech Spikes – simple technology tests that prove or disprove whether a technical solution will work.

Viability looks at the idea from a business lens. Will it save more money than it costs to implement? Will it retain more customers? Will it help acquire new customers? How long will it take to implement? What training will your team need, if any, to put the new idea in the market?

Building the Right Thing

At the end of the Design Sprint, your business will have enough information regarding Desirability, Feasibility and Viability to decide whether or not you should invest in an idea – and enough customer feedback to understand how strongly they feel about your proposal.

This ensures your business will invest in building the right thing – and avoid spending time and resources on ideas that don’t deliver customer and business value.

Why This Matters

Your competitors do not have the same direct and unfettered access to your customers that you have. Your access enables you to find out your customers’ unique needs and pains, and tailor your solution to fit – using a Design Sprint.

Building the right thing for your customers is key. Building the right thing makes your business “sticky” by giving your customer base more reasons to remain with you – even with new alternatives emerging in your market.

This article was written by Lukas Bower (@lukasbower) Managing Director at Industrie&Co Australia. As the payment landscape continues to evolve with new technologies, new payment providers and new customer requirements, it has become increasingly evident that financial institutions must ensure they continually assess whether their products and services are meeting the needs of their market.

The implications of ignoring these ‘disruptions’ is the risk of falling behind the masses and losing out to adaptive competitors.

Responding to the Threat

Indue has partnered with Industrie&Co to enable a major Australian retailer to bring an unprecedented product into the Australian market, which is a great example of responding to the ever-advancing demands of the industry.

Interested to learn about how you can compete with industry disruptors? Join Indue’s Chief Commercial Officer, Dave Hemingway as he hosts an audience with Industrie&Co to dive deeper into the practical applications of design sprint methodology.

When

Thursday, November 14th, 11.00am AEDT

Industrie&Co is an Innovation and Technology Consultancy. With offices in Sydney, Melbourne, Hong Kong and Singapore, Industrie&Co helps Financial Services companies identify and build winning product ideas – from Design Sprint through to launch. Industrie&Co has a strong relationship with Indue, and can help implement next-generation payment solutions. To find out how, please get in touch and share your vision with us.

Industrie&Co is an Innovation and Technology Consultancy. With offices in Sydney, Melbourne, Hong Kong and Singapore, Industrie&Co helps Financial Services companies identify and build winning product ideas – from Design Sprint through to launch. Industrie&Co has a strong relationship with Indue, and can help implement next-generation payment solutions. To find out how, please get in touch and share your vision with us.